India's Cashless Revolution: Digital Payments, Democracy

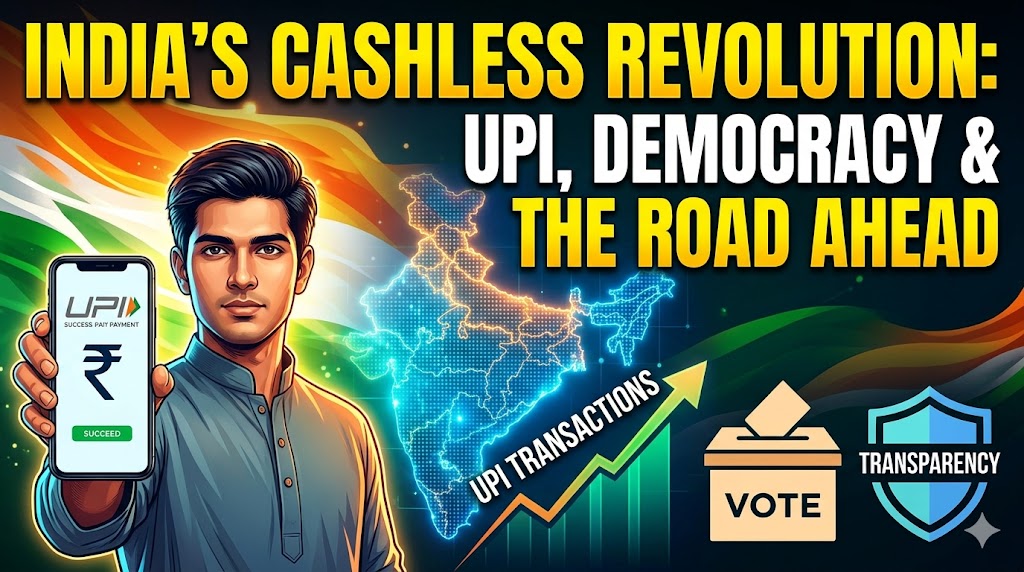

India stands at the forefront of a global digital payments transformation. What began as a bold policy push has evolved into one of the world's most successful fintech stories. With the Unified Payments Interface (UPI) handling billions of transactions monthly, the dream of a cashless India is no longer distant rhetoric but a tangible reality reshaping everyday commerce, governance, and even democratic processes.

From bustling urban markets to remote villages, digital wallets and instant transfers have reduced reliance on physical cash. Yet, questions persist: Is India fully prepared for a cashless economy? How has the 2016 demonetization influenced black money and transparency? And what role does this play in strengthening democracy through better political funding oversight?

This article examines these interconnected themes with balanced insights, drawing on recent data and real-world developments. It offers a structured analysis suitable for readers, policymakers, and students preparing for group discussions.

The Journey to Cashless India: From Demonetization to Digital Dominance

The push toward a cashless society gained momentum with the November 2016 demonetization. Overnight, high-value currency notes were invalidated to curb black money, counterfeit currency, and terror financing. While the move caused short-term disruptions—long bank queues, temporary economic slowdown, and job impacts in cash-dependent sectors—it accelerated digital adoption.

Post-demonetization, the government promoted initiatives under Digital India, including UPI launch in 2016. This interoperable system allows seamless bank-to-bank transfers via mobile apps using a Virtual Payment Address (VPA), without sharing sensitive details.

Today, the results speak volumes. In March 2026, UPI recorded over 22.64 billion transactions worth approximately ₹29.53 lakh crore. For the full year 2025, UPI processed around 228.5 billion transactions valued at nearly ₹299.74 trillion—a 33% year-on-year volume growth. UPI now accounts for roughly 81-85% of retail digital payments in India, making it the world's largest real-time payment system by volume.

E-wallets like Paytm, PhonePe, and Google Pay, integrated with UPI, have further democratized access. Features such as UPI 123PAY enable even feature-phone users in low-connectivity areas to transact via IVR or missed calls, bridging the urban-rural divide.

This growth reflects more than technology; it signals behavioral change. Merchants increasingly display QR codes, and consumers prefer instant, paperless payments for everything from street vendors to utility bills.

Is India Ready for a Cashless Economy? Opportunities and Ground Realities

India has made impressive strides, but readiness varies across regions and demographics.

Strengths and Opportunities:

Scale and Inclusion: Over 500 million active UPI users and millions of QR codes deployed. Initiatives like Payment Infrastructure Development Fund (PIDF) have expanded acceptance points, especially in rural areas.

Economic Benefits: Digital payments enhance transparency, reduce leakage in government schemes (e.g., Direct Benefit Transfers), boost tax compliance, and formalize the economy. They lower transaction costs for businesses and enable better credit access for small merchants.

Innovation Edge: UPI's success positions India as a global exporter of payment technology, with linkages in countries like Singapore, UAE, and France.

Financial Literacy Push: Programs under Digital India and centers for financial literacy have trained millions, particularly empowering women and youth in smaller towns.

Challenges Remaining:

Digital Divide: Rural areas still face inconsistent internet, electricity, and smartphone penetration. Many elderly citizens and low-income groups prefer cash for its familiarity and tangibility.

Cyber Security and Fraud: Rising digital transactions bring risks of phishing, SIM swaps, and data breaches. While NPCI and RBI have introduced AI-based monitoring and awareness campaigns, building public trust remains key.

Infrastructure Gaps: Not all merchants, especially micro-vendors, are fully onboarded. Cash continues to dominate certain informal sectors.

Literacy and Awareness: Financial and digital literacy gaps persist, leading to hesitation or errors in transactions.

Overall, India is not fully "cashless" yet—cash still circulates for small-value or emergency needs—but the trajectory is clear. Projections suggest digital payments could triple in volume by 2030, with UPI playing a central role. A balanced hybrid model (cash + digital) may suit India's diversity better than an abrupt zero-cash shift.

Transition and Gaps. A conceptual image contrasting rapid digital payments adoption in modern urban markets (left) with the persistent infrastructure and awareness gaps facing rural communities (right), illustrating that while India is making progress, full 'readiness' varies by region.

For group discussions (GD points on "Is India Ready for the Cashless Economy?"):

Pros Side: Highlight UPI stats, reduced black money circulation in formal channels, job creation in fintech, and global leadership.

Cons Side: Discuss rural exclusion, fraud risks, initial demonetization pains, and the need for robust infrastructure.

Balanced View: Emphasize phased implementation, public-private partnerships, and continuous literacy drives as the way forward.

Data Points: Cite UPI's 730 million daily transactions in peak months and its dominance in micro-payments.

Black Money, Demonetization, and Transparency Gains

Demonetization aimed to flush out unaccounted wealth held in cash. While 99%+ of old notes returned to the banking system (limiting direct black money seizure), indirect benefits emerged: increased tax filings, formalization of savings, and a surge in digital trials that make evasion harder.

Black money persists, often in real estate, gold, or offshore assets rather than pure cash hoards. Surveys indicate public concern remains high, with many believing undeclared wealth still fuels property deals. However, tools like GST, Aadhaar-linked accounts, and digital payments have improved tracking and reduced anonymity in transactions.

The shift has made the economy more traceable, aiding authorities in curbing corruption and terror funding indirectly.

Digital Payments and Democracy: The Transparency Link

In a vibrant democracy like India, economic tools influence governance. Digital payments foster accountability by creating auditable records, reducing cash-based leakages in welfare schemes, and enabling data-driven policy.

Political funding remains a critical intersection. Elections in India involve massive expenditures, traditionally reliant on cash or opaque channels. The now-scrapped Electoral Bonds scheme (2018-2024) aimed to formalize donations but faced criticism for lacking donor transparency, potentially enabling undue influence. The Supreme Court struck it down in 2024, emphasizing voters' right to information under Article 19(1)(a).

Today, discussions focus on reforming political funding for greater openness—perhaps through enhanced disclosure norms, state funding models, or digital contribution platforms. A cashless ecosystem supports this by minimizing untraceable cash flows, aligning economic modernization with democratic integrity.

American media coverage often contrasts India's democratic complexities with China's authoritarian efficiency, sometimes highlighting India's digital leap as a soft power strength amid geopolitical tensions. Such global narratives underscore how India's cashless push showcases democratic resilience through inclusive technology rather than top-down control.

Creative Ad Concepts for Promoting Cashless India

To sustain momentum, creative campaigns can inspire adoption:

1. Scan to Empower – A short video showing a rural woman vendor switching from cash to UPI QR, gaining financial independence and educating her family. Tagline: "One Scan, Infinite Possibilities."

2. Cashless = Carefree – Humorous animation depicting the chaos of carrying cash (lost wallets, counting notes) versus seamless UPI payments. End with real user stories from tier-2 cities.

3. UPI for Unity – Highlight cross-regional transactions: a North Indian sending money instantly to family in South India. Emphasize national integration and reduced barriers.

4. Youth-Focused Reel Series– Gen Z creators demonstrating quick UPI hacks for college canteens or gig economy payments, with trending music and calls to "Go Digital, Grow India."

5. Elder-Friendly – Simple tutorials via community radio or TV, featuring trusted figures explaining safety features and UPI 123PAY for non-smartphone users.

These ads should blend emotion, simplicity, and data (e.g., "Join 500 million+ users") to build confidence without overwhelming audiences.

The Road Ahead: Building a Sustainable Cashless Society

India's digital payments ecosystem is projected to grow exponentially, with forecasts of hundreds of billions in transactions by 2030. Success depends on addressing gaps: expanding rural broadband, strengthening cybersecurity, and tailoring solutions for diverse populations.

Government, banks, fintech firms, and civil society must collaborate. The digital rupee (e₹) pilot and credit-on-UPI features signal further innovation.

Ultimately, a cashless (or less-cash) India promises greater inclusion, efficiency, and transparency—strengthening both the economy and democratic fabric. Challenges exist, but the progress since 2016 demonstrates resilience and ingenuity.

As citizens, staying informed, adopting safely, and advocating for inclusive policies will determine how fully this revolution benefits all.

Transparent Democracy. A conceptual illustration visualizing a cashless ecosystem supporting democracy. Opaque, cash-based political funding streams (flying out of a traditional box) are transformed into auditable, digital records that strengthen voters' right to information and ensure transparent governance.

Conclusion

India's cashless journey intertwines technology, policy, and societal change. From demonetization's bold experiment to UPI's global benchmark status, the country has rewritten payment norms. While not yet fully ready for a pure cashless economy, the foundation is solid, with digital tools enhancing transparency in public life and political processes.

Continued focus on literacy, infrastructure, and trust will determine the pace. In a democracy as diverse as India's, this revolution offers a path to equitable growth—where every transaction tells a story of progress.