RBI Payments Vision 2028: India’s Global Digital Dominance

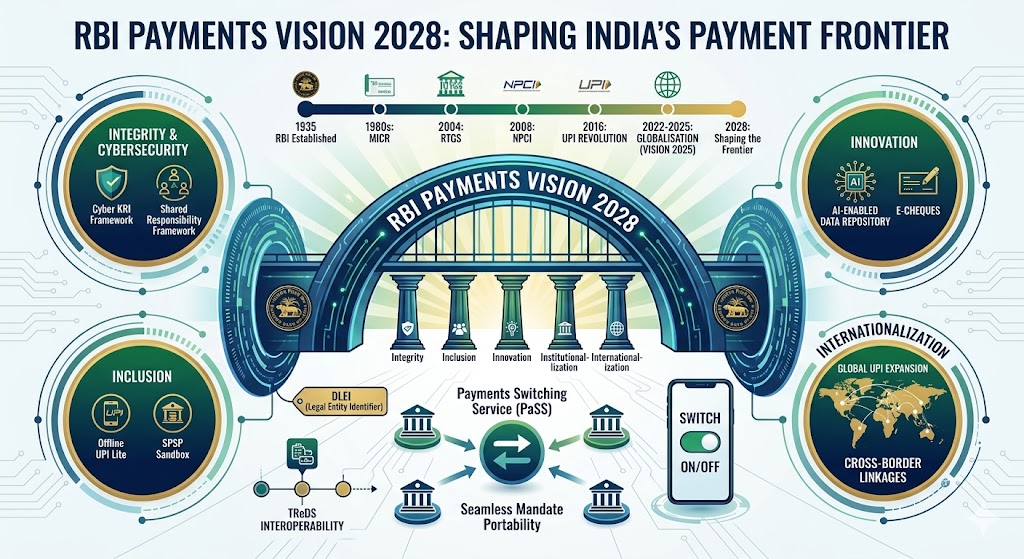

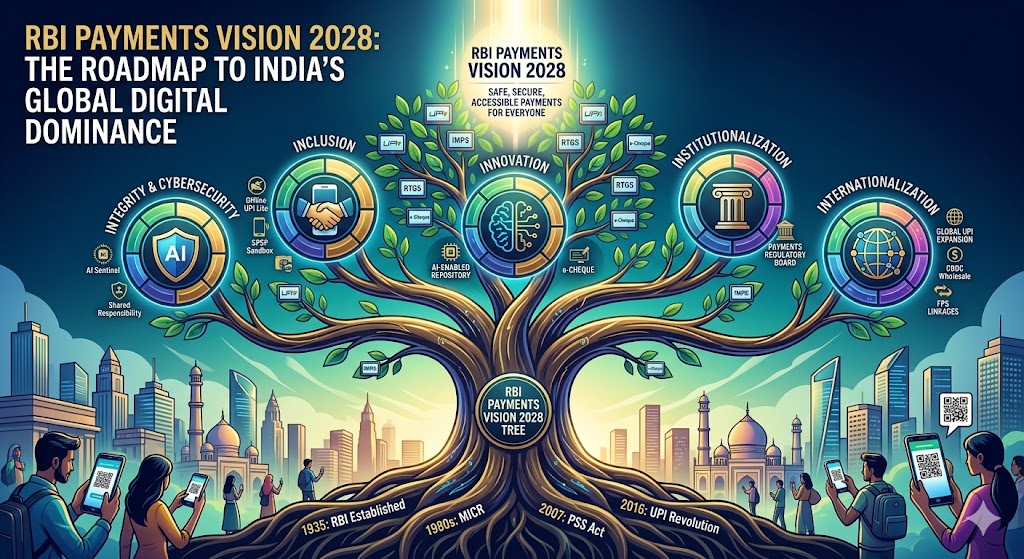

India’s financial landscape is undergoing a metamorphosis that is being studied by central banks across the globe. The RBI Payments Vision 2028, titled "Shaping India’s Payment Frontier," is not merely a policy document; it is a declaration of India’s intent to lead the Fourth Industrial Revolution in finance.

Building upon the successes of the RBI Payment Vision 2025, the new 2028 roadmap shifts focus from volume-driven growth to resilience, integrity, and internationalization.As we navigate the complexities of a $5 trillion economy, the "RBI Payments Vision 2028" serves as the lighthouse for every stakeholder, from the rural farmer using UPI to the multinational corporation settling billion-dollar cross-border trades.

I: The Historical Tapestry of the Reserve Bank of India

To understand the magnitude of the RBI Payments Vision 2028, one must look back at the nearly century-long evolution of the Reserve Bank of India. The story of the RBI is not just the story of a central bank; it is the story of India’s economic sovereignty and its transition from a physical, paper-led economy to a global digital leader.

1. The Pre-Independence Era (1935–1947)

The inception of the RBI was recommended by the Hilton Young Commission in 1926. However, it wasn't until April 1, 1935, that the Reserve Bank of India commenced operations under the RBI Act, 1934. Initially established as a shareholders' bank with a share capital of ₹5 crore, its primary mandate was to regulate the issue of bank notes and maintain reserves to ensure monetary stability.

During this period, the "payment system" was rudimentary, relying heavily on physical metallic coins and high-denomination paper notes. In 1946, just a year before independence, the RBI executed its first major policy intervention by demonetizing ₹1,000 and ₹10,000 notes to curb unaccounted wealth—a precursor to the modern regulatory rigor we see today.

2.Post-Independence and Nationalization (1947–1969)

Following India’s independence, the RBI was nationalized on January 1, 1949, under the Reserve Bank (Transfer to Public Ownership) Act, 1948. This transformed the RBI from a colonial institution into the guardian of a nascent democracy’s financial health.

The 1950s and 60s were characterized by the expansion of the banking network into rural India. The RBI played a pivotal role in the State Bank of India (SBI) creation and later the nationalization of 14 major commercial banks in 1969. During this era, payments were entirely paper-based, with the "Cheque" being the king of transactions. The clearing process was manual, often taking weeks to settle funds between cities.

3. The Technological Awakening (1970s–1990s)

The 1980s marked the first "tech" spark within the RBI. Recognizing the inefficiency of manual clearing, the RBI introduced Magnetic Ink Character Recognition (MICR) technology. This allowed for the automated sorting of cheques, drastically reducing settlement times.

The 1991 economic reforms acted as a catalyst. As the Indian economy opened to global markets, the need for faster fund movement became critical. This led to the development of:

Electronic Clearing Service (ECS): Introduced in the 1990s for bulk payments like salaries and utility bills.

The Board for Regulation and Supervision of Payment and Settlement Systems (BPSS): Established to provide dedicated oversight to the evolving payment landscape.

4. The Modern Digital Revolution (2000–2020)

The turn of the millennium saw the most rapid shift in RBI history.

RTGS & NEFT: In 2004, the RBI launched the Real-Time Gross Settlement (RTGS) system for high-value transactions, followed by National Electronic Funds Transfer (NEFT). This moved India from "days" to "hours" for fund transfers.

The PSS Act, 2007: This landmark legislation gave the RBI the statutory power to regulate all payment systems in India.

Birth of NPCI (2008): In a visionary move, the RBI and IBA (Indian Banks' Association) set up the National Payments Corporation of India (NPCI). This entity became the laboratory for innovations like IMPS, RuPay, and eventually, the Unified Payments Interface (UPI) in 2016.

5. Transitioning to Vision 2028

Between 2020 and 2025, the RBI successfully navigated the global pandemic by pushing digital payments to record highs. The RBI Payment Vision 2025 focused on "E-payments for Everyone, Everywhere, Everytime."

Now, the RBI Payments Vision 2028 stands on the shoulders of these giants. It moves beyond just domestic availability, aiming to integrate Artificial Intelligence, launch e-cheques, and establish the Indian Rupee as a preferred currency for cross-border payments.

> Historical Note:The transition from the 1935 physical ledger to the 2028 AI-enabled payments repository represents a 10,000x increase in transaction velocity, a feat unmatched by any other major central bank globally.

Shaping the Future of Global Finance: RBI Payments Vision 2028

II: The 5 Strategic Goalposts of Vision 2028

The RBI payment system vision for 2028 is anchored by five core pillars, often referred to as the "5 Is":

1. Integrity: Strengthening the Trust Factor

Integrity is the bedrock of any financial system. Under the RBI cybersecurity payments mandate for 2028, the central bank is introducing a Cyber Key Risk Indicators (KRI) framework.

Continuous Monitoring: Non-bank Payment System Operators (PSOs) will now be monitored in real-time.

Shared Responsibility Framework: In a landmark move, both the issuing bank and the beneficiary bank will now share liability for unauthorized transactions, forcing a collaborative approach to fraud prevention.

2. Inclusion: Leaving No One Behind

The RBI vision 2028 summary emphasizes that digital payments must reach the last mile.

Offline Payments: Enhancements to "UPI Lite" and offline card solutions to cater to regions with poor connectivity.

SPSP Recognition: The small payment system provider RBI framework allows niche players to operate in rural "sandboxes," fostering local innovation.

3. Innovation: From AI to E-Cheques

Innovation is the engine of the payments vision 2028.

RBI AI Payments Repository: The creation of a unified, AI-enabled repository will allow for advanced data analytics, helping the RBI spot systemic risks before they manifest.

E-Cheques: Replacing the traditional paper-based process, e-cheques will offer the legal finality of a cheque with the speed of digital processing.

4.Institutionalization: Robust Governance

The RBI has replaced the old Board for Regulation and Supervision of Payment and Settlement Systems with a more empowered Payments Regulatory Board (PRB). This body ensures that the rbi vision document 2028 remains a living, breathing strategy.

5. Internationalization: Global UPI Expansion

The RBI cross border payments strategy is perhaps the most ambitious. By 2028, the RBI aims to link India’s Fast Payment Systems (FPS) with major global corridors, reducing the cost of remittances to well below the G20 target of 3%.

III: Revolutionary New Rules and Features

The rbi new rule 2028 set includes several consumer-centric features:

1. Payments Switching Service (PaSS)

One of the most discussed features in the .rbi payments vision 2028 india report is bank account portability. Through PaSS, customers can migrate all their standing instructions and mandates to a new bank account with a single click.

2. The Universal "Switch On/Off" Facility

Building on the success of card controls, the rbi vision 2028 introduces a universal toggle. Users can now enable or disable any digital payment mode (UPI, IMPS, AePS) via their banking app, providing an immediate defense against phishing.

3. Domestic Legal Entity Identifier (DLEI)

To manage risks in the B2B sector, the RBI is studying the implementation of a Domestic Legal Entity Identifier (DLEI). This unique code for non-individuals will ensure total transparency in high-value corporate transfers.

The Five Pillars of India’s Financial Sovereignty

IV: The Role of AI and Data Analytics

The RBI AI payments repository is a game-changer for 2028. By centralizing payment data, the RBI can:

1. Predict Fraud Patterns: Use machine learning to identify "mule accounts" instantly.

2. Optimize Liquidity: Help banks manage their cash reserves more efficiently based on real-time spending trends.

3. Enhance Transparency: Provide the public with deeper insights into the health of the digital economy.

V: Supporting Small Providers and MSMEs

The small payment system provider rbi framework is designed to help startups. By operating in a perpetual regulatory sandbox, these providers can test solutions for India upi vision 2028 without the burden of full compliance until they reach a significant scale.

Furthermore, the interoperability of TReDS platforms (Trade Receivables Discounting System) will ensure that MSMEs can get their invoices financed across any platform, improving cash flow for the backbone of the Indian economy.

Part VI: Comparison – Vision 2025 vs. Vision 2028

| Feature | RBI Payment Vision 2025 | RBI Payments Vision 2028 |

|Primary Goal| Volume and Accessibility | Resilience and Global Linkage |

| Fraud Management | Awareness and Reporting | AI-Repository & Shared Liability |

| Cheque System| CTS (Image Based) | E-Cheques (Fully Digital) |

| Global Presence | UPI Pilot projects | Universal FPS Linkages |

| User Control | Card-based On/Off | Universal Payment On/Off |

The Future of Currency: A New Era of Trust and Digital Integration

The RBI Payments Vision 2028 is a testament to India's journey from a cash-dependent society to a global digital pioneer. By 2028, we will see an India where cross-border payments are as easy as a local UPI scan, where bank account portability is a reality, and where AI-driven security makes digital transactions safer than physical cash.

As the RBI continues to innovate, the focus remains clear: Integrity, Inclusion, and Innovation. This vision document ensures that India doesn't just participate in the future of finance—it defines it.