India's Excise Duty Cuts on Petrol & Diesel Amid Oil Crisis.

In late March 2026, as geopolitical tensions in West Asia escalated with the US-Israel conflict involving Iran, India took decisive fiscal action to shield its economy and citizens from volatile global energy prices. On March 26-27, the central government reduced the special additional excise duty (SAED) on petrol from ₹13 to ₹3 per litre and eliminated it entirely on diesel (from ₹10 per litre). This move, effective immediately, was designed not to slash pump prices outright but to offset surging crude costs, prevent under-recoveries for state-owned oil marketing companies (OMCs), and curb inflationary pressures.

For an international audience unfamiliar with India's complex fuel pricing regime, this intervention highlights a key feature of emerging-market energy policy: the use of taxation as a buffer against external shocks. India, the world's third-largest oil importer, relies on imports for over 85-90% of its crude needs, with a significant portion historically transiting the Strait of Hormuz. Disruptions there—now near-effective closure due to heightened risks—have driven benchmark oil prices sharply higher, threatening supply chains worldwide.

This article examines the mechanics of excise duties on petrol and diesel, recent LPG price adjustments, the historical context of India's fuel taxation, immediate domestic impacts, broader global ramifications, supporting research, and prospective changes. Drawing on current data as of late March 2026, it provides a balanced, forward-looking analysis for policymakers, investors, and observers abroad.

LPG gas price high amid oil crisis

The Structure of Fuel Pricing in India: Excise Duty Explained

Retail prices of petrol and diesel in India comprise multiple layers: the base cost of crude (landed after refining), OMC margins, central excise duties (including basic excise duty, SAED, agriculture infrastructure and development cess, and road/infrastructure cess), state value-added tax (VAT), and dealer commissions. Excise duties form a substantial portion—often 30-40% of the final price—making them a flexible tool for the central government.

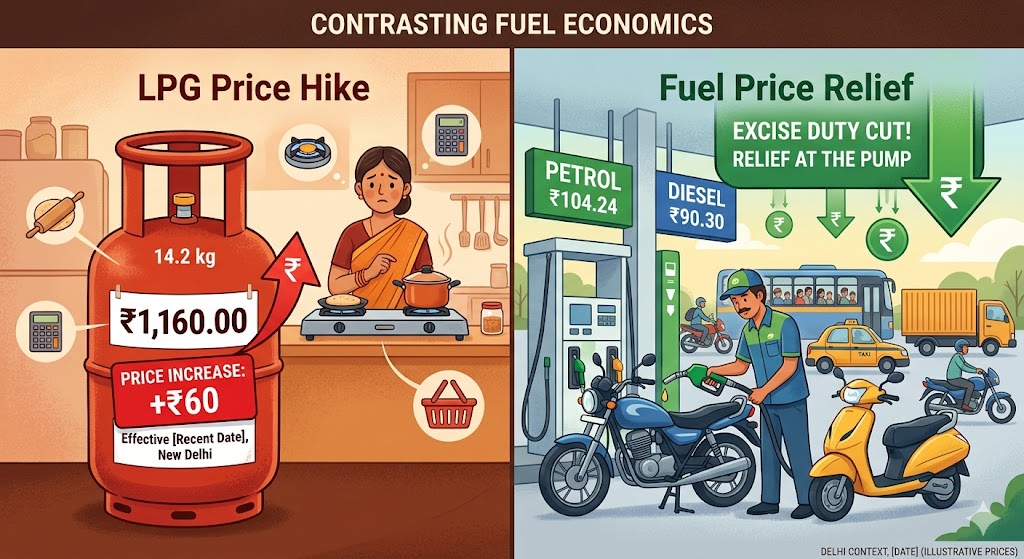

As of the latest revision, the total central excise incidence stands at approximately ₹11.90 per litre for petrol (₹1.40 basic + ₹3 SAED + ₹2.50 cess + ₹5 road cess) and ₹7.80 per litre for diesel. Retail prices in major cities like Delhi remain stable at around ₹94.77 for petrol and ₹87.67 for diesel, unchanged post-cut, as the duty relief absorbs crude cost increases rather than passing savings to consumers.

This calibrated approach differs from fully liberalized markets in the US or Europe, where pump prices fluctuate daily with global benchmarks. India's policy prioritizes stability to protect inflation-sensitive sectors like transport, agriculture, and household budgets. However, it places fiscal pressure on the government, which forgoes revenue while OMCs avoid losses estimated at ₹24 per litre for petrol and ₹30 for diesel at peak crude levels.

Historical Evolution of Excise Duties on Petrol and Diesel

India's excise duty trajectory reflects pragmatic fiscal management amid oil price cycles. When the current government assumed office in 2014, rates were modest: ₹9.48 per litre on petrol and ₹3.56 on diesel. Between November 2014 and January 2016, duties rose nine times (total +₹11.77 on petrol, +₹13.47 on diesel) to capture windfall gains from plummeting global crude prices, boosting collections dramatically from ₹99,000 crore in 2014-15 to over ₹2.42 lakh crore by 2016-17.

Subsequent adjustments included minor cuts in 2017-18 (₹2 then ₹1.50 per litre) during price peaks, followed by hikes in 2019-2020 (₹2 in July 2019; ₹3 in March 2020 and a record ₹10/₹13 in May 2020 during COVID-induced low crude) to fund infrastructure amid revenue shortfalls. A notable relief came in May 2022 with ₹8 and ₹6 reductions per litre on petrol and diesel, respectively, amid post-pandemic recovery.

By April 2025, SAED had climbed to ₹13 on petrol and ₹10 on diesel. The March 2026 cut reverses this partially, echoing past patterns: raise duties during benign global conditions to build fiscal buffers, then ease them during crises. This "counter-cyclical" strategy has enabled massive infrastructure investments but drawn criticism for burdening consumers during high-price periods.

The March 2026 Cuts: Details, Rationale, and Companion Measures

Announced via a finance ministry notification on March 26, 2026, the ₹10 per litre SAED reduction on both fuels addresses acute OMC under-recoveries triggered by the West Asia crisis. Oil Minister Hardeep Singh Puri noted the government absorbing a "huge hit" on revenues to prevent losses from spiraling. Concurrently, windfall taxes were reimposed on diesel exports and aviation turbine fuel (ATF) at elevated rates (e.g., 21.5% on diesel exports in some reports), alongside higher excise on ATF exports to prioritize domestic supply and deter hoarding.

The fiscal cost is significant: an estimated ₹70 billion revenue loss per fortnight (net ₹55 billion after export tax offsets), or roughly ₹7,000 crore in just 15 days. This equates to potential annual impacts in the range of ₹1.75 lakh crore if sustained, challenging the government's 4.3% fiscal deficit target for FY 2026-27. Bond yields rose in response, reflecting market concerns over borrowing needs.

Critically, retail prices did not fall; the cut maintains equilibrium. This "hidden subsidy" via tax foregone benefits consumers indirectly while shielding OMCs—key to ensuring uninterrupted fuel availability amid panic buying reports.

LPG Pricing Dynamics and Recent Adjustments

While petrol and diesel garnered headlines, LPG (liquefied petroleum gas)—vital for 300 million+ Indian households—saw its own turbulence. On March 7, 2026, domestic non-subsidized 14.2 kg cylinder prices rose ₹60 to ₹913 in Delhi (first hike in nearly a year, following a smaller April 2025 increase of ₹50). Commercial 19 kg cylinders jumped ₹115 to ₹1,883. These adjustments stem from the same global factors: Saudi CP benchmark rises (up ~21% in recent periods) and Strait of Hormuz shipping disruptions inflating import costs. India imports ~60% of its LPG.

Subsidies under Pradhan Mantri Ujjwala Yojana (PMUY) for low-income users remain at ₹300 per cylinder but are capped at nine refills annually (down from 12), with total subsidy outlay revised upward to ₹12,000 crore for FY 2025-26. The government extended booking periods to 25 days to curb hoarding. For foreign observers, this underscores India's dual-track pricing: market-linked for general users, subsidized (yet increasingly targeted) for the vulnerable, balancing fiscal prudence with social welfare amid 39% effective price relief for PMUY beneficiaries in recent years.

recent inflation affects the world

Domestic Economic Impacts

The duty cuts provide immediate relief by containing transport and logistics costs, which ripple into food inflation, manufacturing, and services. Without them, petrol could have approached ₹100+ in many cities, exacerbating pressures on a $4 trillion economy growing at 6-7%. However, revenue foregone may necessitate higher borrowing or spending cuts elsewhere, potentially crowding out infrastructure or welfare programs.

Research from bodies like the State Bank of India and rating agencies (e.g., ICRA) models oil shocks: sustained $100/barrel crude could trim GDP growth to 6.6% (from baseline ~7%) and lift inflation to 4.1%, widening the current account deficit to 1.9-2.2% of GDP. Fertilizer subsidies could balloon by ₹200 billion. OMCs' improved margins support stock performance and dividend flows to the exchequer, but prolonged high crude risks under-recoveries if duties are not adjusted further.

Global Ramifications and Interconnections

India's policy reverberates internationally. As a major demand driver (consuming ~5.5-6 million barrels/day of oil), price stability sustains consumption, cushioning global markets from sharper demand destruction. Conversely, aggressive duty hikes elsewhere could suppress imports, easing pressure on benchmarks like Brent.

The Iran conflict's Strait of Hormuz disruptions—accounting for ~20% of global oil and 19% of LNG trade—have tightened supplies, elevating prices 30-50% in affected regions and triggering inflation worldwide. Higher energy costs inflate freight, chemicals, and consumer goods, hitting export-oriented economies from Europe to East Asia. India's import diversification (increasing Russian and US crude shares) and strategic reserves mitigate some risks, but its actions exemplify how large importers' fiscal tools influence global price discovery.

Broader effects include accelerated energy transitions: higher prices incentivize renewables, EVs, and LNG alternatives. For India, this aligns with net-zero ambitions by 2070, though short-term reliance persists. Globally, it underscores vulnerability in chokepoint-dependent supply chains, prompting calls for diversified routes and stockpiles.

Research Insights on Fuel Prices and Economic Outcomes

Empirical studies reinforce these dynamics. World Bank analyses of LPG subsidy reforms (e.g., PAHAL direct benefit transfers) highlight efficiency gains but note implementation challenges in targeting. Econometric models from Indian think tanks show a 10% fuel price rise correlates with 0.5-1% headline inflation spikes, disproportionately affecting rural and low-income groups.

International comparisons (e.g., IMF papers) position India's excise flexibility as superior to rigid subsidy regimes in oil-producing nations, avoiding fiscal cliffs. However, research warns of "Dutch disease" risks if revenue dependence on fuel taxes distorts diversification. In the 2026 context, IEA forecasts global oil demand growth at a modest 640 kb/d for the year (down from prior estimates), with non-OPEC+ supply rising 1.1 mb/d—yet geopolitical premiums could sustain volatility.

Future Outlook and Potential Changes

Looking ahead, outcomes hinge on conflict resolution. A swift de-escalation could see oil prices moderate toward $70-80/barrel averages projected by some analysts (e.g., J.P. Morgan's bearish $60 scenario tempered by risks), allowing India to restore duties gradually. Prolonged disruption might trigger further interventions: deeper subsidies, accelerated biofuel blending, or import duty tweaks.

Policy evolution likely includes greater market liberalization, digital pricing transparency, and green hydrogen/LNG infrastructure push. LPG may see more frequent monthly revisions, with subsidies increasingly digitized and capped. For global audiences, India's experience offers lessons in hybrid energy governance—blending state intervention with market signals—amid energy security imperatives.

Challenges remain: fiscal sustainability, rupee volatility (a weaker currency amplifies import costs), and equity in burden-sharing. Optimistically, sustained high prices could catalyze faster adoption of renewables, positioning India as a leader in the global energy transition.

Conclusion

India's March 2026 excise duty reductions on petrol and diesel exemplify agile governance in turbulent times. By absorbing costs centrally, the government safeguards consumers and economic momentum without distorting retail signals entirely. Paired with LPG adjustments, this reflects a nuanced strategy balancing immediate relief against long-term fiscal health.

Globally, the episode illuminates interconnected vulnerabilities: from Hormuz chokepoints to inflationary spillovers. As research underscores, such shocks test resilience but also spur innovation. For foreign stakeholders—be they investors eyeing Indian markets or analysts tracking energy geopolitics—the takeaway is clear: India's fuel policies are not merely domestic levers but pivotal influences on worldwide stability and the pace of sustainable energy shifts. Monitoring developments through 2026 will reveal whether this intervention marks a temporary buffer or a pivot toward enduring reform.